Blog

NC State Financial Mathematics Highlighted by Leading Financial Careers Website

April 27, 2023

The NC State Master of Financial Mathematics (MFM) program was recently highlighted in an article published by the globally known leading financial services career website efinancialcareers.com.

The article discusses the value and return on investment of master’s degree programs in financial engineering (MFE) or financial mathematics as an alternative to traditional master’s programs in finance. The authors utilized the latest graduation data from publicly available employment reports to compare outcomes of specialized master’s programs like the MFM program at NC State.

As stated in the article “MFE graduate salaries rose at all colleges in the past two years. The largest jump in base salary was at NC State University, with the current average of $118k up $31k on two years ago.” This is an impressive 35% increase in base salary secured by NC State graduates within this two-year span.

In addition to an increase in base salary, NC State also consistently maintains a 100% full-time employment rate of graduates up to 6 months following graduation, including the recent graduating class of 2022.

The MFM Program at NC State is proud to be cited by this internationally recognized news source and be included on a list of prestigious universities such as NYU, Berkley, Carnegie Mellon, Columbia, and Georgia Tech.

NC State MFM program director, Dr. Tao Pang said “I am thrilled to see that more and more companies recognize the value of our students. We will continue to maintain an updated curriculum and meet the market demands. I am confident that our students at NC State will have continued success and be competitive in the job market.”

Click here to view the complete article. For more information regarding the MFM program at NC State, please contact program director, Dr. Tao Pang at tpang@ncsu.edu.

Using QuantConnect for a Quantitative Trading Course

Robert Graham Carroll | April 25, 2023

The QuantConnect platform allowed graduate students in the Master of Financial Mathematics program at North Carolina State University to test the durability of historical investment strategies. In Graham Carroll’s Quantitative Trading Strategies and Technology course, the class developed an algorithm based on Joseph D. Piotroski’s fundamental analysis strategy “Value Investing: The Use of Historical Financial Statement Information to Separate Winners from Losers.”

QuantConnect’s platform provided an ideal coding environment for the class to develop code together within minutes of the class starting, avoiding having to set up local environments. Interacting with the LEAN framework required students to expand their existing programming abilities, while the Backtesting environment allowed them to focus on how their trading hypothesis performed.

Students identified equities using Piotroski’s alpha signals and optimized positioning strategies. After defining the strategy’s universe filter, students focused on developing an algorithm with two static variables. After discussing how the portfolio would perform with different values for these static variables, students were able to use QuantConnect’s Parameter Optimization functionality to backtest several hundred combinations with just the click of a button.

The ability to run backtests for combinations of multiple variable values defined directly from the platform was a particularly powerful tool. Students were able to see how different combinations of values affected the performance of the trading strategy, providing them with valuable insights into the behavior of the strategy.

The course focused on improving programming skills by utilizing the collaborative and interactive environment for developing code. Version control using GitHub was introduced as an additional collaboration tool for the group project. By learning version control on GitHub, students will have the opportunity to build up their portfolio and showcase their work to potential employers.

Overall, the QuantConnect platform provided an excellent tool for teaching algorithmic trading in a hands-on and interactive way. The ability to develop and test strategies in a single platform allowed students to see the full picture of how their strategies would perform in the real world. With the help of QuantConnect, students were able to gain a deeper understanding of the complexities of trading and develop valuable skills that will serve them well in their future careers.

ESG Strategies: burden or opportunity?

Hans Castro | Feb. 1, 2022

ESG has become a trending topic recently in the past few years, and the concerns about the topic have spread all around the world. The financial industry, companies in general and investors have been paying attention to it and we have seen a big movement towards ESG implementation. Even though ESG is not an asset class it can become a blind spot if not overseen and therefore finance and risk professionals must be aware of it.

First, ESG stands for Environmental, Social and Governance, so far there’s not a unique definition or a single rule on how it must be measured however, companies are disclosing information on how they handle these topics and, investors and consumers are attentive. When available, the ESG reports are disclosed with the financial reports making of this document a complement to regular analysis, it provides a new perspective on risks that were not considered before. Thanks to the disclosure, some companies have created ESG Scores and by the end of the last fiscal year (2020) there were 3,191 public companies in the United States with an ESG score compared to only 725 in January 2012. It is important to mention that only 4 companies had scores greater than 90: Walgreens Boots Alliance Inc, Microsoft Corp, Owens Corning and 3M Co. There is a lot of room for improvement .

Second, the financial industry is a big player in terms of ESG because can provide the resources to make the ESG movement feasible and can influence its clients to take ESG issues into consideration. There are some global efforts to respond to this challenge in the world, i.e., the finance initiative of the United Nations (UN) has created the Principles for Responsible Banking with 275 signatories which represent US$42 trillion assets and more than 45% of the global banking assets; in the USA there are 7 signatories banks including Citi and The Goldman Sachs Group, Inc.

ESG shouldn’t be just an inconvenience but new ways to make a profit or to gather money for green projects to reduce risk. For example, green bonds finance projects aimed at energy efficiency, sustainable agriculture, forestry, clean transportation, etc. By January 2022 just in the US there was U$159 billion in green bonds and in China up to U$176 billion. Big companies like Apple and Bank of America have issued green bonds for US$4.72 billion and U$4 billion respectively.

Due to all these changes, the regulators of the financial industry are getting involved, and I believe that any time soon it will be mandatory. In the United States the topic is still evolving however, just at the end of January 2022, the European Central Bank published the “Climate risk stress test”, a framework to assess quantitively the climate risk.

To conclude, I can be sure that ESG strategies represent an opportunity more than a burden. There is not “one-size fits all” approaches so companies can execute their tailored strategies to create resilience in light of those risk that haven’t been contemplated before. There are financial resources available to accomplish these goals and the sooner action is taken the better considering upcoming future regulations. Our blue planet would appreciate it, too.

Turn an Internship into a Full-time Job

(Nov. 5, 2020)

Mr. Joshua Johnstone, an alumnus from our program, who now works as a Senior Associate Research Statistician Developer at SAS, joined us at the MFM Roundtable on Nov. 5, 2020.

First, Joshua talked about how he chose the electives while he was in the program. Then he shared his interview experience for his internship at SAS. It turned out that most of the interview questions were technical questions, as the HR team was not there. He said that it would be more non-technical questions if the HR team is on the interview committee. He told the students not to be discouraged by a letter of decline, and just keep trying.

Regarding how to turn an internship into a full-time job, Joshua shared some tips. The first is that don’t be afraid of asking questions, but you should make an attempt to solve the problem first. Another thing is to build professional relationships with your co-workers. Finally, it is totally ok to ask for what you want. Let them know you want to continue to work for them. As an intern, you need to keep asking yourself, ‘Where can I contribute? Where can I add value?’

Joshua also talked about his recent project on risk modeling and the technical skills needed.

Maintain Your Network

(Oct. 28, 2020)

Ms. Maria Emilia Calderon, an alumna who currently works a Quantitative Financial Analyst at Mazars, UK, is our guest speaker for the MFM Roundtable on Oct. 28, 2020. Maria was also one of our FM Ambassadors while she was in the program.

At the Roundtable, Maria shared her experience on how she found her summer intern at Morgan Stanley in New York City and how she secured the fulltime job at Mazars. She thinks it is very important build your network, and it is also very important to maintain your network. Actually, it was a connection at Mazars that Maria built before she came to NC State that leads to her current full-time job at Mazars in the UK. Maria also answered questions from students such as how to establish and maintain a connection through Linkedin.

In addition, Maria talked about how her typical works were like and what skills are needed. She gave her overviews on the job opportunities in credit risk, marker risk and date science in finance. Finally, Maria discussed the challenges and changes brought to her job by the COVID-19.

Set up Your Career Goals

(Oct. 22, 2020, article by Huixuan Bao)

Mr. Pengfei Xiong, an alumnus from our program, who now works in quantitative risk and stress-testing team as an assistant vice president at Citi Group, shared some of his experience on job hunting and gave some advice from a previous ambassador’s point of view at the MFM Roundtable on October 22, 2020.

Pengfei shared his experience to get an internship at Genworth. He once did a presentation to a guest speaker from Genworth at the FM seminar. Then he was offered an internship at Genworth under the supervising of the guest speaker during the next summer. Based on this experience, Pengfei highly recommended the students to actively attend the seminars or roundtable meetings held by the program and connect with the guests since that would be a good start. Besides, Pengfei also suggested that first year students could extend their graduate timeline to two years to better prepare for job searching and should set up their career goals early, because different jobs have different focus and may need different skillsets. Pengfei also answered questions from students regarding his current work.

A Reflection on Interviewing

(Oct. 15, 2020, article by Matthew Puksta)

Kartheek Manavarthi, graduated in 2019 from the Financial Mathematics program. Currently working as a Risk analyst for First Citizen’s Bank, Kartheek shared his experience with the students regarding how to interview for a job and provided key insight from an international student applying in America at the MFM Roundtable on Oct. 15, 2020.

Kartheek covered how he found a job and utilized mutual connections and group events such as job fairs to build personal connections. Kartheek gave suggestions of how to build business connections at a personal level using commonalities, mutual research, topics of interest, and by showing interest in an individual. Lastly he touched on the importance of continued applications until securing a job, and how an internship can lead to a full time position in the quantitative finance field. Kartheek also took questions from the audience on related topics and his experiences at work and in applying for positions.

Do Not Hold Yourself Back

(October 8, 2020. Article by Zheng Liu)

Mr. Juman Ahmed, an alumnus of our program who works at the Federal Reserve Bank at Minneapolis, shared his experience in getting start of his career at the MFM Roundtable on Thursday, October 8, 2020.

Before Juman took the current job, he worked at CISCO as a summer intern and a part-time employee at CISCO. The project he participated in at CISCO contains multiple parts including data cleaning and model development. What he gained while working at CISCO was not only the implications of his knowledge but also the importance of communication. Good communication skills can help you find proper recourses for the project. For example, asking your manager questions before starting will help you understand the project better.

Juman told the students that do not hold back yourself at work. According to him, if you finish the assignment before the deadline, do not just stay back and relax. Instead, you should reach out to your manager ask for more to do.

When it comes to the experience of searching for an internship, Juman told students it is better to use different resumes for different jobs. In addition, do not to get disappointed when receiving a rejection letter. Often you will receive a hundred rejection letters at the same time you receive one offer.

Juman also answered questions from students regarding his opinions on coursework and projects.

Seizing Every Opportunity

(Sep. 30, 2020, article by Huixuan Bao)

Mr. Daniel Peters, an alumnus from our program who now works at the State Employee’s Credit Union as a financial modeling analyst, gave a presentation at the MFM Roundtable on Wednesday, September 30, 2020. He shared his recent experience on developing a pre-provision net revenue (PPNR) model.

Before joining SECU, Daniel held two internships in Lincoln Financial Group and Willis Towers Watson. At Lincoln Financial Group, he worked as a life actuarial intern, and at Willis Towers Watson, he worked as a retirement actuarial intern. When it comes to the experience of his success in finding internships as well as full time jobs, Daniel advised the students to apply everywhere possible since you never know when and where opportunities will appear. He also suggested that reading recent articles from FED and stress testing documents from consulting companies is useful for preparing interviews.

Preparing Your Interview, from the Opposite Side of the Table

(September 25, 2020. Article by Zheng Liu)

Mr. Yuhong Fu, an alumnus from the program, now assistant VP at Citibank, shared his experience and opinions with current students in preparing for an interview from the company’s perspective, at the MFM Roundtable on September 25, 2020.

With his relative working experience in Equifax and PNC bank, Yuhong joined the Quantitative Risk and Stress Testing Group at Citibank after graduating from the MFM program in December 2019. Combining his journey of looking for jobs, he summarized the fundamental factors from the interviewer’s perspective when selecting candidates. After sharing his experience, Yuhong answered the students’ questions on a range of topics, from solving the technical questions to utilizing different experiences to land the job. Finally, he encouraged students to take the initiative for applying and networking.

Career Workshop by Dr. Paul Miceli

January 24th, 2020: Career Workshop run by Dr. Paul Miceli from Genworth Financial

- Dr. Paul Miceli is the Organizational Learning and Development Manager at Genworth Financial. Dr. Miceli has worked at Genworth for five years and has served in his current role for almost two years.

- Dr. Miceli received his PhD in 2012 from UNC Chapel Hill, in Social Psychology with a concentration in Quantitative Psychology.

- Dr. Miceli spoke about the importance of developing professional networks and how best to develop those networks within the finance industry.

- Dr Miceli additionally spoke about the importance of breaking bad networking habits and how to improve your individual skills to make networking more efficient.

Career Workshop by Credit Suisse Team

Nov 15th 2019: Excellent workshop conducted by our guests from Credit Suisse.

- John Viegas, is Raleigh site lead for Group Operations within the COO division. He is also the Global Head of Oversight & Control, the Americas Head of Securities Settlements and the Group Operations Raleigh Site Lead.

- Rahul Nath, Vice President, Trade Settlement Systems. He discussed about the current challenges he sees in his work and how technology helps to resolve them.

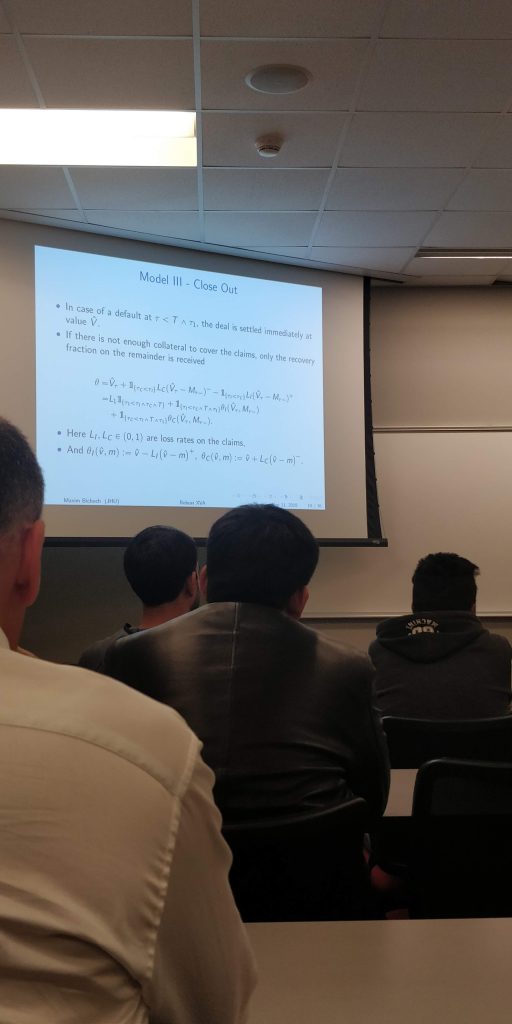

Session on Robust XVA

Nov 11th, 2019: Dr. Maxim Bichuch, from John Hopkins University gave an overview of Robust XVA. He illustrated the reasons for the introduction of Valuation Adjustments as a consequence of the financial crisis of 2007-9 and further elaborated on an arbitrage-free framework for robust valuation adjustments.

Session on Overview of US Financial System

Nov 8th, 2019: Mr. Yao Song, Vice President from Local Government Federal Credit Union, gave an excellent (non-technical) overview of the US financial system. Yao Song, CFA, FRM is currently Vice President of Financial Risk at Local Government Federal Credit Union in Raleigh, North Carolina. In this role, he primarily oversees the modeling, reporting, and management of the credit union’s financial risk exposures (interest rate risk, liquidity risk and credit risk). In addition, he leads the effort on capital management, financial forecasting and analysis, and strategic balance sheet management. He previously worked at RBC Bank (USA), a subsidiary of Royal Bank of Canada. He is a graduate of UNC-Chapel Hill and Northwestern University.

FM Alumni Reunion (2019)

at Raleigh & New York City

Chapter 1: 4th October 2019: The alumni of the Financial Math program came together to meet old friends, connect with the students, and share their experiences in the industry. The meet commenced with some of the alumni taking us through their journey starting from their background. This was followed by two-panel discussions which helped the students understand the most needed technical skills and the hot topics in the industry presently.

- Panel Discussion I: Ken Kalsch, Le Li, Samuel Knox, Albert Hopping, Aisha Barnes

- Panel Discussion II: Jeffery High, Jeff Scroggs, Joshua Johnstone, Natalia Sanchez.

The reunion ended with an evening reception at the Aloft hotel.

Chapter 2: 10th October 2019 After the reunion in Raleigh, there was a meet and greet session at the Merchants River House in New York with the alumni working there. It was a fun get together and great to connect with them. Thank you all for taking the time out to be there and making it a success!

Bank of America’s Classroom Chat Session

Sept 27th, 2019: NC State Financial Mathematics program had the amazing opportunity of having

- Abigail Roberson – Campus Recruiter at Bank of America,

- Vijayendra Tanwar -Alumni of the FM program and Managing Director at Bank of America,

- Yanglin Yu – Senior Data Scientist at Bank of America and

- Zachary Small – Global Quantitative Analytics Associate at Bank of America

The session kicked off with a short and exciting coding challenge followed by an insightful presentation on the various career opportunities at Bank of America.

Session on ‘Stochastic Games with Delays: A Toy Model’

Sept 20th, 2019: NC State Financial Mathematics program had the privilege to host Prof. Jean-Pierre Fouque, the founder of our program back in 2002 who is currently a distinguished professor and the co-director of Center for Financial Mathematics and Actuarial Research at UC Santa Barbara. He is also the editor-in-chief of the SIAM Journal on Financial Mathematics. He gave an interesting and enthralling session on ‘Stochastic Games with Delays: A Toy Model’.

Session on ‘Accelerating DFAST Modeling via Genetic Algorithms’

NC State Financial Mathematics program was honored to host Mr. Joe Zweier, FRM from State Employees’ Credit Union (SECU) on 13th September 2019 for a session on ‘Accelerating DFAST Modeling via Genetic Algorithms’.

Fall 2019 New Graduate Students Orientation

August 20th 2019

The NC State Financial Mathematics Program welcomes the new Graduate Students starting Fall 2019.

CECL and Credit Risk Modelling Summit 2019

April 11-12th, 2019 – By: Rohit Khurana

The NC State Financial Mathematics Program along with Industry Leaders and Regulators have organized the CECL and Credit Risk Modelling Summit from Apr 11-12th 2019 at Raleigh, NC. This was a huge success with overwhelming participation of 120+ delegates representing 30+ organizations.

This comprised of:

- Regulatory & Legislative Updates by members from Federal Reserve, OCC, and US Congressional Staff, with an excellent Q&A opportunity

- Discussion on Calculation Methodologies

- Holistic Approach to CECL and Stress Testing

- Healthy Discussion among participants from 30+ organizations (comprising of Banks, Credit Unions, Industry Leaders, Regulators, etc.)

- Poster Presentation by Graduate Students

“Thank you all so much for holding this event. It is really helpful. Thanks again for providing the opportunity for us to talk to industry experts and regulators face to face.”- Yahui Bai, Quantitative Analyst at BB&T

More about the summit can be referenced here: https://financial.math.ncsu.edu/cecl-summit/

Spring Break Get-Together

Apr 5th, 2019 – By: Amoolya Prakash

During spring break, the class of financial mathematics decided to meet up and this time it wasn’t to have any group study or to discuss projects or assignments. We wanted to get to know one another beyond our financial acumen and intelligence. So, thanks to the enterprising members of the batch, we met up at Historic Yates mill park, which historically also, was the centre for social gathering. We then proceeded to Lake Wheeler and let our hair down to play volleyball, (which was a first for a lot of us).

Panel Discussion & Networking – Spring’19

Feb 15th, 2019 – By: Rohit Khurana

During Spring’19 FIM 601 class, on 15th Feb we had two Panel Discussions on two important career topics i.e. a) Quantitative Finance in 21st Century: Tools, Techniques and the Industry and b) Financial Risk Management in Banking and Insurance Industry: Evolution or Revolution? Panellists comprised of six seasoned industry leaders from the field of data science and risk management and panels were facilitated by the students of the MFM program.

First panel had discussed in detail on the topic “Quantitative Finance in the 21st Century”, tools & technique, key shift in decision-making post-2008 crisis era, etc. This comprised of John Hanna, AVP from Credit Suisse, Shinese Bennett, Risk Analyst at First Citizen Bank (FCB), and Albert Hopping, Senior Manager in Risk Consulting at SAS and facilitated by Garrett Mills, student of MFM program, class of Spring’19, was excellent as a facilitator and did a fantastic job in engaging the Speakers and concluding well within the stipulated time frame allowing the forum to engage any open questions.

The second panel on the day addressed another interesting topic “Financial Risk Management in Banking and Insurance Industry: Evolution or Revolution?” This discussion was as good as the first one as this highlighted the paradigm shift in the industry for Risk Management roles. This panel comprised of Dr. Ram Valluru, Director, ERM & Reinsurance Analytics, at Genworth, Ratnakar Chitturi, from Credit Suisse, and Tianhao Lu, Risk Consultant from Financial Risk Group (FRG) and facilitated by Zezhou Wang, student of MFM Program.

Overall everyone enjoyed the discussion and interaction. Tanmay Sah, FM Ambassador, felt this was one of the successful and efficient events of the semester demonstrating the full strength of students’ enthusiasm and their zeal.